Courtyard by Marriott – Redwood City: HVS Market Pulse: Silicon Valley

Home to numerous high-tech corporations and startup companies, Silicon Valley encompasses the southern portion of the San Francisco Bay Area. As defined by the 2017 Silicon Valley Index, this region covers the cities in San Mateo County and Santa Clara County. The index also incorporates portions of Alameda County, including the cities of Fremont, Newark, and Union City, as well as Scotts Valley in Santa Cruz County. For purposes of this article, the greater Silicon Valley area will follow the aforementioned definition, with the exception of Scotts Valley. This article will primarily focus on new hotel development, and hotel trends within the greater Silicon Valley area.

Silicon Valley has previously been noted as one of the fastest-growing urban economies in the United States. Unemployment in this market has continued to decline since the recession, closing out 2016 at 3.8%, down from 4.3% in 2015 and 5.3% in 2014, approximately 1.1% lower than the national average. However, venture capital investment in the region has begun to show some slowdown, with deal activity at an eight-quarter low in Q4 2016, and remaining relatively flat in Q1 2017. [1] According to REIS, the supply for office space has begun to outpace demand, with vacancy rates projected to increase to 17.2% in 2017, up from 16.8% in 2016 and 15.9% in 2015. However, average asking lease rates continue to improve and are currently at the highest levels achieved during the last decade, with sustained growth anticipated through the near term. Meanwhile, airlift throughout the greater San Francisco Bay Area has also improved, with year-over-year increases in passenger traffic at the airports in San Francisco, San Jose, and Oakland. Major indicators for the second quarter of 2017 reflect continuation of these trends, which bodes well for the market’s lodging industry.

Commercial Developments

Tech companies continue to dominate the local economy of Silicon Valley, with a number of key employers expanding and investing in new office space and operations. Although some construction is still ongoing, Apple’s new $5-billion headquarters, located approximately one mile east of the current campus in Cupertino, opened in April 2017. When completed, Apple Park will house more than 12,000 employees in a four-story circular building that totals roughly 2,800,000 square feet.

In June 2017, Google announced tentative plans to develop up to six million square feet of office and R&D space with Trammel Crow near the Diridon Transit Station in San Jose. The San Jose City Council has agreed to negotiate exclusively with Google for the sale of 16 parcels on Montgomery and Autumn Streets. While negotiations have been tentatively scheduled through July 2018, an application to begin the project’s development and land-use entitlements following the completed sale could also take an extended period of time, with construction not likely to commence for at least another two years.

On the north side of Silicon Valley, Facebook, located in Menlo Park, is also looking to expand with its new Willow Campus. In its initial plans submitted to the Menlo City Council in early July 2017, the mixed-use development integrates its office expansion plans with a grocery store, a pharmacy, and 1,500 housing units, of which 15% will reportedly be offered at below-market rates. Facebook has reportedly pre-leased 700,000 square feet of office space currently under construction adjacent to the 250-room Hotel Nia, Autograph Collection, which is also under construction near Marsh Road and U.S. Highway 101.

In May 2017, LinkedIn presented plans for a new East Whisman office campus in Mountain View, totaling nearly 1.1 million square feet. The initial plans call for the construction of three new, six-story buildings, as well as merging several existing office buildings and parcels into the site, creating a new headquarters for the company.

Peninsula Corridor Electrification Project – Caltrain Modernization

Concurrent with improvements to the greater San Francisco Bay Area’s economy, Silicon Valley has realized a substantial increase in population over the last decade. According to the 2017 Silicon Valley Index, Silicon Valley’s population (San Mateo & Santa Clara Counties) grew 7.5% between 2010 and 2016, more than 2% higher than the average population growth for the state of California. As the local population continues to grow, Caltrain has experienced a similar increase in ridership, with strong year-over-year increases in weekday commuters between 2011 and 2016.

To accommodate these increases in ridership, as well as to mitigate delays and improve service, Caltrain has announced a $2-billion modernization program that includ es electrifying 51 miles of track, converting diesel-hauled to Electric Multiple Unit (EMU) trains, and implementing a new control system; benefits includ e more frequent trains, as well as doubling ridership capacity. When completed in 2020/21, the project will upgrade the performance, efficiency, capacity, safety, and reliability of Caltrain’s commuter rail service. Although the line is anticipated to be utilized primarily by residents, it should ease traffic congestion and facilitate transportation throughout Silicon Valley and the San Francisco Peninsula.

Hotel Supply

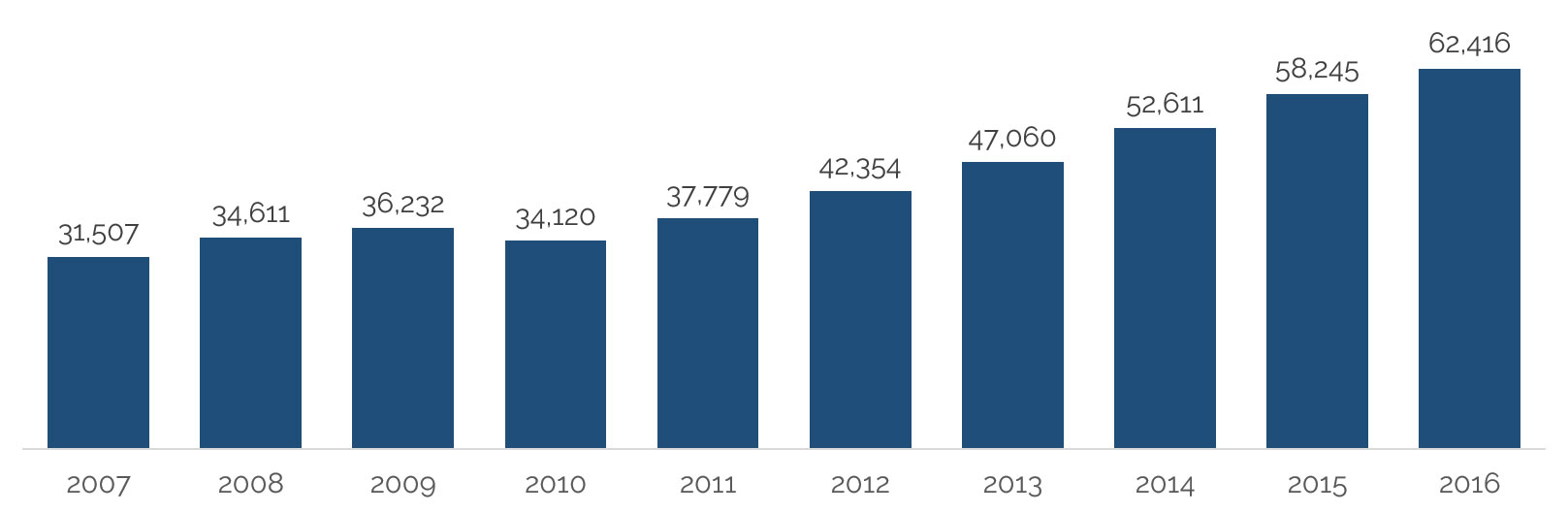

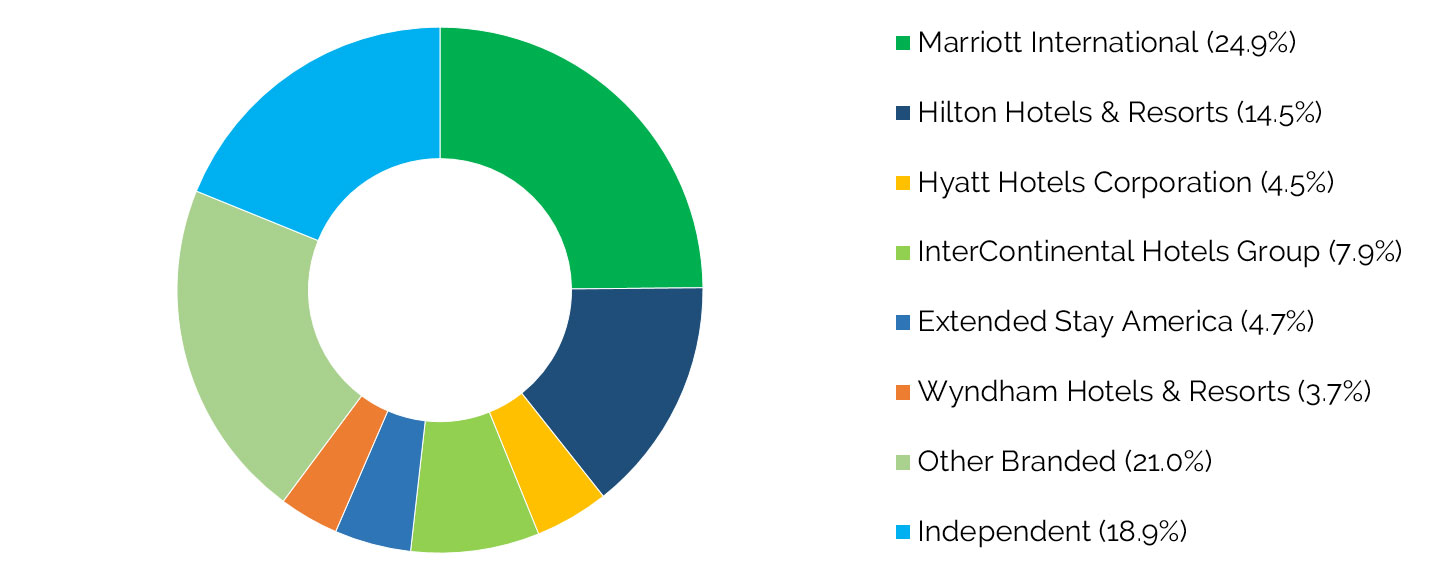

According to Smith Travel Research (STR), Silicon Valley’s hotel inventory currently comprises roughly 46,800 rooms across nearly 420 properties. Of this set, approximately 60% belong to a brand or major parent company, with the remaining 40% operating as independent hotels. Of the roughly 38,000 branded rooms, Marriott International and Hilton Inc. combined operate approximately 48%. InterContinental Hotels Group, Hyatt Hotels Corporation, Wyndham Hotels & Resorts, and Extended Stay America also have sizeable representation in the market, ranging between roughly 4% and 8% market share.

Based on recent HVS surveys of market participants, the greater Silicon Valley market achieved significant year-over-year RevPAR growth between 2010 and 2016. However, occupancy has begun to moderate downward, attributed to the entrance of new supply. Furthermore, San Francisco’s Moscone Center is currently under renovation, resulting in less compression and fiercer competition for meeting and group demand between hotels in the San Francisco and Silicon Valley submarkets. Similarly, average rate growth has also experienced a modest slowdown, partially attributed to the normalization of rates in the first quarter of 2017 because of the Super Bowl’s inflated rates during the same period last year, as well as further discounts to attract and maintain group demand. However, with occupancy close to capacity on Monday through Thursday nights, local operators will likely continue to pursue a rate-driven strategy through the near term.

The greater Silicon Valley market continues to be driven by strong weekday demand from major corporate accounts, such as Google, Apple, Facebook, Oracle, LinkedIn, eBay, PayPal, and Samsung. While weekend demand continues to remain a challenge in most submarkets throughout Silicon Valley, with rates discounted significantly to sustain occupancy, Levi’s Stadium drew a crowd of 71,088 fans for Super Bowl 50, selling out a number of hotels throughout the San Francisco Bay Area. Reportedly, the event attracted over one million visitors to the Bay Area in late January/early February 2016.

The following table illustrates a list of new hotels that have opened since January 2014.

As previously described in our 2015 article, the market is starting to see a significant increase in new supply, particularly in the select-service and extended-stay products that cater to Silicon Valley’s strong commercial and group market segments.

Opened in September 2015, the Aloft Santa Clara is located on the far north side of the city, proximate to the 430,000-square-foot America Center office development. The Clement Hotel Palo Alto is a high-end, exclusive boutique hotel located on the western edge of the city. Featuring a unique luxury product, this property is owned and managed by Pacific Hotel Management, which also owns and operates the adjacent full-service Westin and Sheraton properties. One of the first hotels to represent the brand’s new Del Sol Prototype, the La Quinta Inn & Suites Morgan Hill features a distinct design meant to maximize revenue per square foot while maintaining a competitive cost per key. After numerous delays, the AC Hotel by Marriott opened in early 2017 in Downtown San Jose. This property is the first of several AC Hotels currently under development in the greater San Francisco Bay area. Opened in March 2017, the Courtyard by Marriott Redwood City was developed by OTO Development; with five other hotels, including three Marriott- and two Hilton-affiliated properties, in various stages of development in just the greater Silicon Valley market alone, it’s no surprise that the Spartanburg-based company recently was named Marriott International’s 2017 CONNECT Developer of the Year and Hilton’s Focused Service Developer of the Year.

New Supply

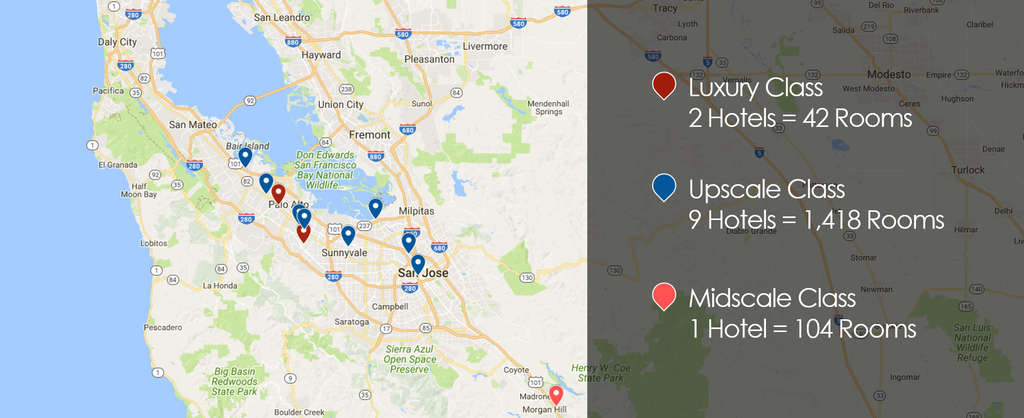

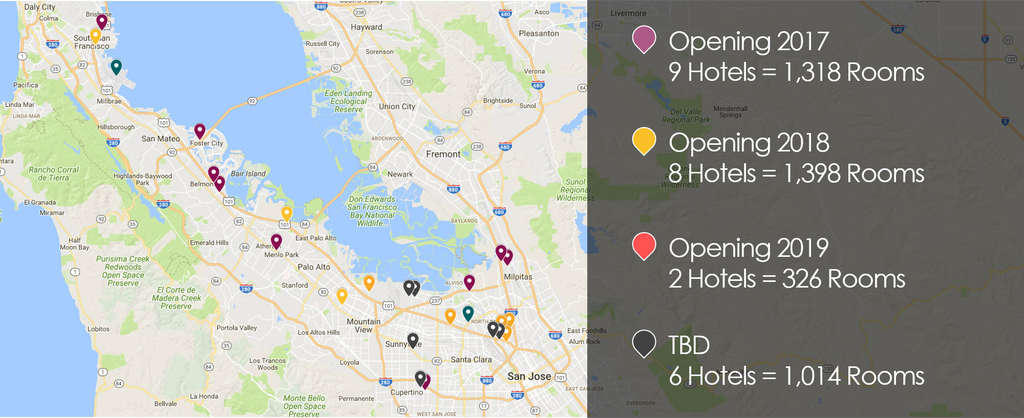

As Silicon Valley maintains its status as one of the top-performing lodging markets in the United States, developers continue to propose new projects, despite the high barriers to entry and challenging entitlement processes in California. Some of the proposed projects have recently broken ground, while others have received preliminary approval, received entitlements, and/or are facing substantial hurdles that will require a lengthy development timeline. Of the 85 hotels (roughly 13,150 rooms) that have been proposed for development, 25 projects (approximately 4,000 rooms) have begun site work, broken ground, or are currently under construction.

With numerous commercial and residential projects under development in the greater San Francisco Bay Area, construction costs have been increasing significantly year-over-year. According to JLL’s 2016 Q4 U.S. Construction Outlook, cities in the Bay Area trail only New York in terms of building costs. As such, many hotel developers have turned toward branded limited-service, select-service, and extended-stay properties that favor lower development costs and efficient layouts of the guestrooms, public spaces, and back-of-house areas. Some notable projects currently under construction includ e the following:

Located within the Menlo Gateway mixed-use development, the Hotel Nia, Autograph Collection is a luxury, full-service hotel that is expected to cater to Silicon Valley’s individual business travelers. Managed by Sage Hospitality and offering 20,000 square feet of flexible meeting space, the eleven-story hotel will benefit from its proximity to major employers in San Mateo County, such as Facebook and Amazon, when it opens in early 2018.

The Hyatt Centric is part of the second phase of development at the 56-acre The Village at San Antonio Center. The 168-room hotel is being built in conjunction with two six-story office buildings totaling 448,000 square feet.

The Embassy Suites by Hilton is part of the first phase of the Bay 101 Technology Place development. The seven-story hotel is being built adjacent to site of the Bay 101 Casino relocation. The second phase of development will reportedly includ e a nine-story, 242,000-square-foot office building; a ten-story, 240-room hotel; and an eight-story garage with 1,325 parking stalls.

The Grand Hyatt SFO represents a partnership between the San Francisco International Airport and Hyatt Hotels Corporation. This 351-room hotel will be built on the 4.7-acre site of the former Hilton Hotel that was razed in the mid-1990s. With a ground-breaking ceremony held late June 2017, construction on the new hotel is expected to be completed by July 2019. Located at the entrance of the SFO, the hotel will reportedly be built to LEED Gold standards and feature 15,000 square feet of meeting space, a Grand Club lounge, a full-service spa and health club, and an indoor pool and whirlpool. The hotel will also feature direct access to the airport’s AirTrain light-rail system.

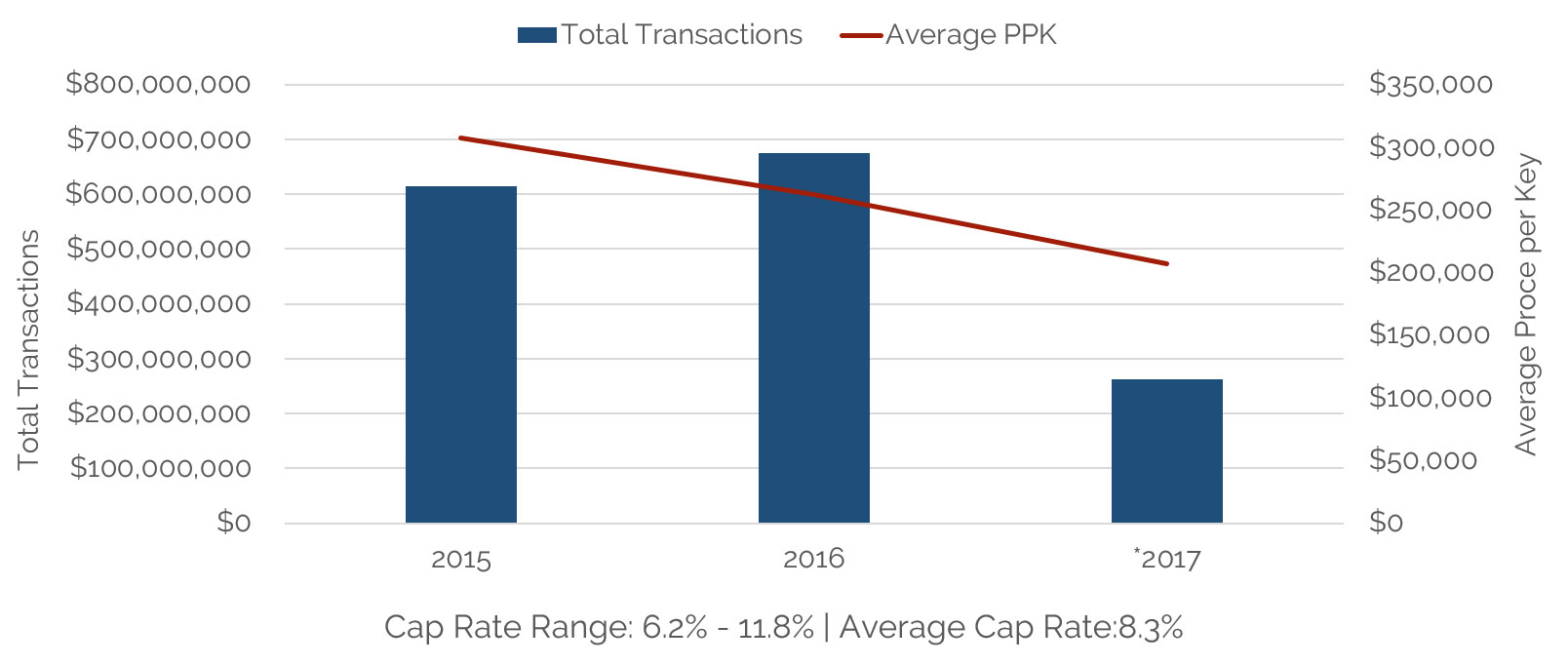

Hotel Transactions

While transaction activity in Silicon Valley has slowed somewhat since the sales frenzy in 2014, a noticeable shift has occurred from the transfer of select-service and extended-stay hotels to full-service properties. As one of the last cities left in the Bay Area with significant portions of land available for new development, San Jose has become Silicon Valley’s newest hotspot. Within the last year, Downtown San Jose has seen the sale of many of its major hotels, including the Hyatt Place, Westin, Hilton, and Marriott. In anticipation of major commercial projects, such as Google’s San Jose Diridon development, real estate investment trusts (REITs), private investment funds, and ownership groups have been quickly targeting these strong, nationally branded hotels that cater toward corporate accounts and group demand.

Other major transactions within the last two years includ e The Blackstone Group’s sale of the Ritz-Carlton Half Moon Bay to China’s Anbang Insurance Group Co. as part of the Strategic Hotels & Resorts portfolio; the Sofitel San Francisco Bay (now rebranded as a Pullman Hotel) purchased by CBRE Global Investments; and the Marriott San Mateo San Francisco Airport, acquired through a subsidiary of Oracle in September 2016. While the sales of select-service assets have slowed significantly, Hersha Hospitality’s 2016 purchase of T2 Development’s Courtyard by Marriott in Sunnyvale at a price of over $500,000 per room illustrates how desirable these efficient, strong cash-flow performing assets continue to be.

As noted in our previous 2015 article, investors that are eager to enter the market are willing to purchase properties needing renovation, repositioning, and possible rebranding, rather than working through the lengthy development process or undertaking riskier new construction projects. Some notable conversions includ e the renovation and rebranding of the former Four Points by Sheraton to the Aloft brand in southwest San Jose, the repositioning of the former Sofitel San Francisco Bay to Accor’s Pullman Hotel, and the conversion of Milpitas’ former Beverly Heritage Hotel to the full-service Sonesta Hotels & Resorts brand. Within Silicon Valley’s limited-service sector, there have been a number of properties that have dropped their brand affiliations to be repositioned as small, boutique hotels. These includ e the conversion of the former Quality Inn to The Nest Palo Alto, the former Days Inn to The Palo Alto Inn, and Mountain View’s former Best Western Plus to the Mountain View Inn. Given the current strong demand in cities such as Palo Alto and Mountain View, some owners are able to eliminate franchise fees and still maintain reasonable RevPAR levels.

The Silicon Valley market remains one of the strongest lodging markets in the United States. Supported by a diverse economy, the market will benefit from the planned developments and expansions at numerous major employers that will improve upon the existing foundation for future economic growth. Despite the anticipation of new supply, record levels of demand have allowed operators to continue to push average rates. Overall, the near-term outlook for the Silicon Valley market remains positive.

20170912